- RE-ITERATE BUY Entry 2.10 – Target – 2.30 Stop Loss – 2.00

- CICT owns and invests in quality income-producing assets primarily used for commercial (including retail and/ or office) purposes, located predominantly in Singapore. As the largest proxy for Singapore commercial real estate, CICT’s portfolio comprises 21 properties in Singapore and two in Frankfurt, Germany, with a total property value of S$22.5bn as of 31 December 2021. CICT is managed by CapitaLand Integrated Commercial Trust Management Limited, a wholly-owned subsidiary of CapitaLand Investment Limited (CLI), a leading global real estate investment manager with a strong Asia foothold.

- Easing of pandemic restrictions from April 2022 to bolster office portfolio. We reckon that the substantial easing of pandemic restrictions in Singapore would provide significant tailwinds to CICT’s office properties. On its office portfolio, anecdotal evidence suggests that the large crowds seen in the core central region on weekdays implies that the return to office community has swelled (22 April 2022: 47%), and should result in greater leasing traction and in turn rental reversions. In addition, we believe that the acquisition of a 70%-stake in CapitaSky on 27 April 2022 will reap immediate benefits to this segment.

- Return of the tourist dollar on eased travel restrictions. According to STB, Singapore clocked 1.5m visitor arrivals in 1H22, more than 12x more on a YoY basis. Meanwhile, 1Q22 tourist dollars climbed to S$1.33bn (+213% YoY) driven by feeder markets such as Indonesia and India. Nonetheless, this is still a far cry from pre-pandemic spending of S$6.6bn in 1Q19. Moving forward, there is increasing optimism that global travel will start to pick up pace and the agency believes that Singapore can expect to receive between 4 to 6 million visitors this year, which would fuel tourism spending particularly along the downtown Orchard road belt.

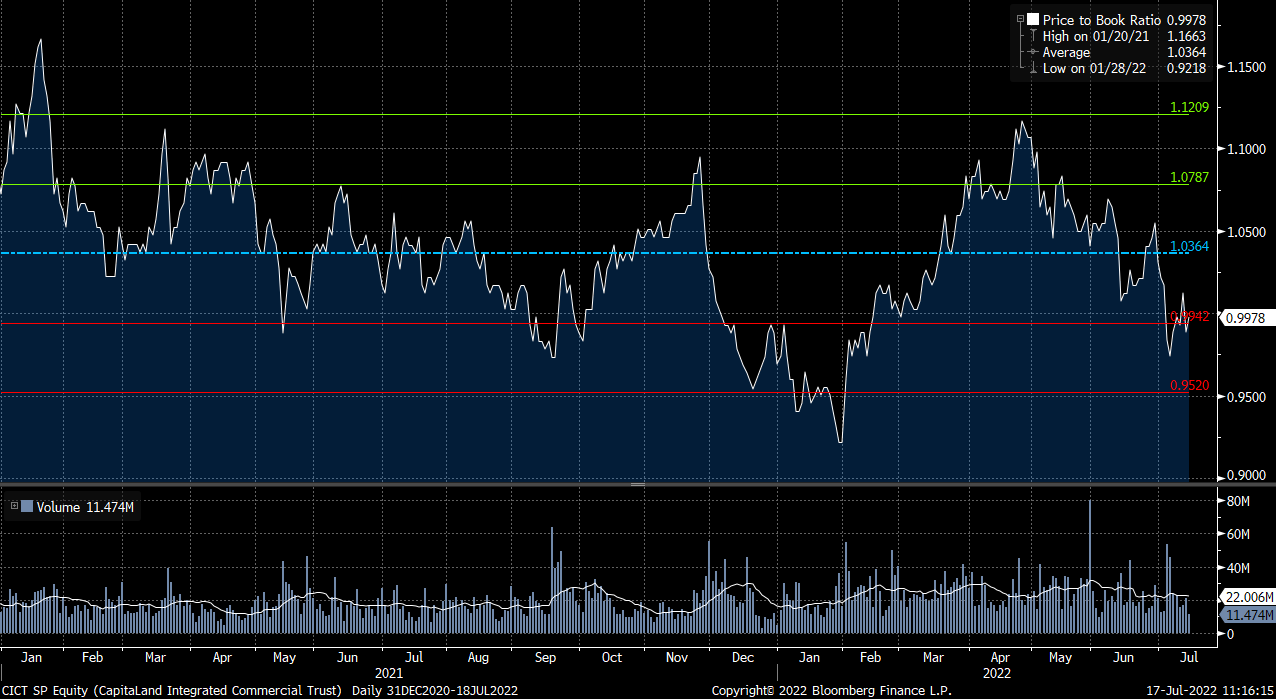

- FY22 results to be fueled by M&As. Recall that in1Q22, CICT already started to see a recovery across its portfolio and reported strong office rental reversion of 9.3%, while its retail rental reversions saw a slight 1.2% increase after excluding Raffles City Singapore’s AEI. The Street is thus overall bullish on CICT’s prospects, with 16/3/1 BUY/HOLD/SELL ratings and an average TP of S$2.45. Based on consensus estimates, FY22F gross revenue and NPI should swell 7.0/8.3% YoY, while distributable income would grow at a faster 12.5% pace. FY22F DPU should come in at 9.3% YoY to S$0.114 apiece due mainly to a larger unit base. We believe that CICT is slightly undervalued now considering that it is currently trading ~1sd away from its post-merger mean of ~1.04x P/B. At current prices, CICT would trade at an attractive 5.4%/5.7% FY22F/23F yield.

(Source: Bloomberg)